The Five Transformative Forces That Are Reshaping Every Industry

A practical framework for identifying the structural forces that determine competitive outcomes, and why most firms are looking in the wrong place

Most strategy frameworks share a limitation: they describe the competitive terrain as it currently exists rather than the forces that are reshaping it.

My research, which analysed 8,430 companies and 9.1 million words of annual reports across 20 years, found that the firms which achieved dominant profit share did so by organising their strategies around long-term external forces. Their competitors, facing the same forces with comparable resources, organised around internal priorities.

The more specific finding was about concentration. The dominant firms did not try to respond to every force in their environment. They emphasised an average of three to four external driver clusters significantly more than their competitors, and they sustained that emphasis across two decades. The small number turns out to be critical. Too many forces leads to diffusion, and what separated 11 firms out of 8,430 from everyone else was selecting the right few and committing to them.

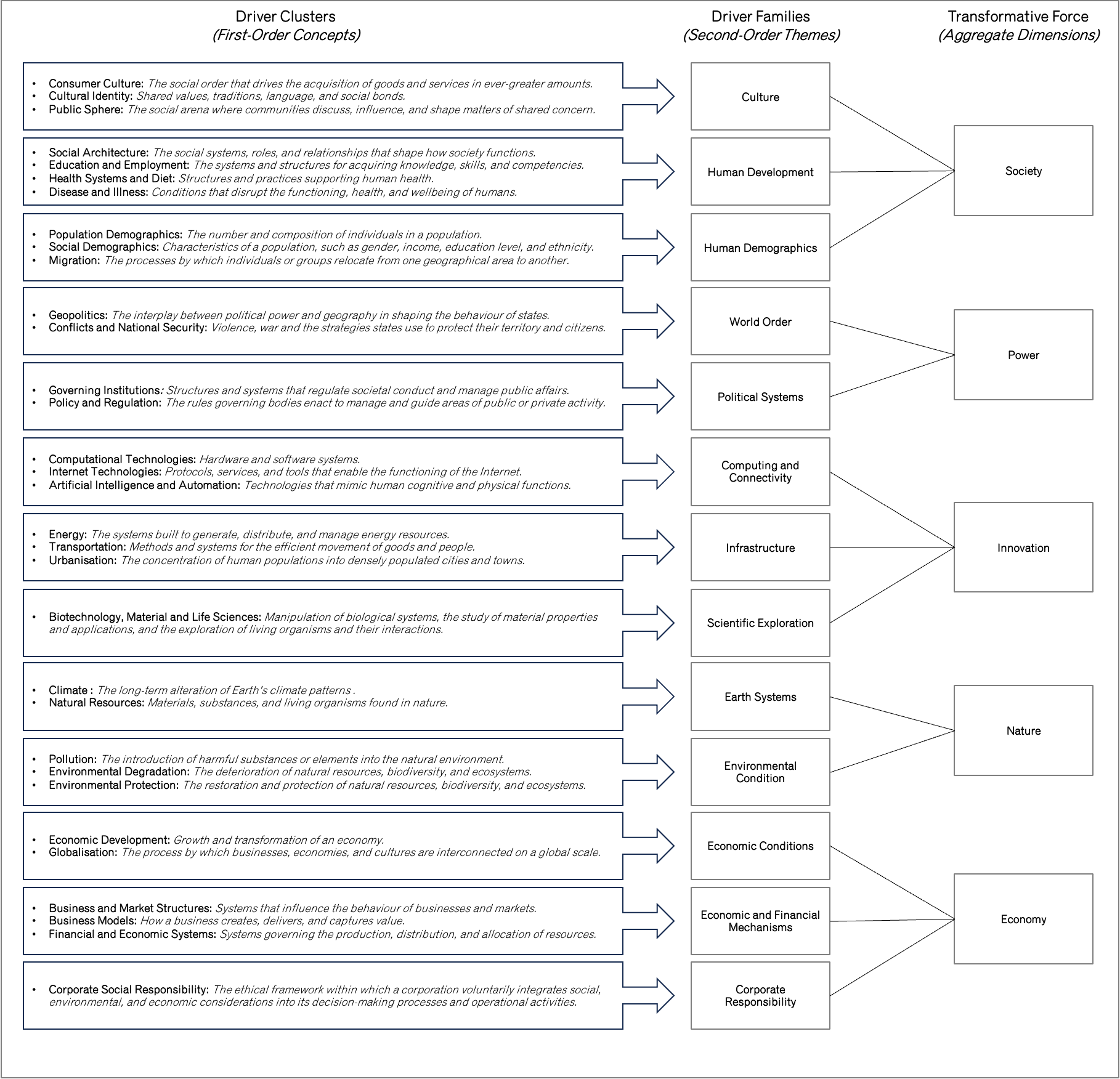

But which forces? The research identified 292 individual drivers of transformation from a systematic review of the academic literature spanning four decades. I organised them into a four-level taxonomy, from individual drivers up through 32 clusters, 13 families, and finally five broad transformative forces. These five forces, Society, Power, Innovation, Nature, and Economy, form the SPINE framework.

These are not competitive forces in the Porter sense. They describe the categories of long-term structural change that operate above the level of any single industry, affecting all industries though not all equally. They are the territory from which strategic themes are drawn, and the convergence points between them are where the strongest competitive positions tend to emerge.

Society

Society reshapes markets through demographics, culture, and human development. Demographics are the slowest-moving and most predictable of all forces, which is precisely why they are so underused in strategic planning.

South Korea’s fertility rate fell to 0.72 children per woman in 2023, the lowest in the world and far below the 2.1 replacement rate. The working-age population has already begun to decline, and projections suggest the country will lose roughly a third of its current population by 2060. Japan, Italy, Spain, and much of Western Europe face the same structural trajectory at different speeds. For any firm that serves families with young children, this is a structural headwind that no product innovation can reverse. But the same demographic shift creates tailwinds elsewhere: eldercare, financial products for longer retirements, and single-person household services will all compound for decades. The same force creates both. The strategic question is which side of it you have chosen to build around.

Cultural shifts move faster. The expectations consumers bring to brands have changed materially over the past decade: transparency about sourcing, environmental commitments, and corporate values has shifted from a niche concern to a mainstream purchasing criterion, accelerated by social media platforms that give communities the tools to organise boycotts and coordinate switching behaviour. Fast fashion illustrates the convergence. Shein grew to become one of the world’s largest fashion retailers by offering extreme speed and extreme price, but its model has attracted sustained regulatory scrutiny in the EU and a consumer backlash from younger buyers who view disposable clothing as incompatible with their values. The strategic implications run in both directions: a firm positioned around sustainability faces a growing tailwind, whilst a firm positioned around volume and disposability faces a headwind that regulatory pressure is accelerating. A cultural shift that would have taken a decade to propagate in 1995 can propagate in two years today.

In the content analysis, this force showed up clearly. Unilever’s annual reports placed significantly higher emphasis on consumer culture and sustainability language than L’Oréal’s across the same 20-year period. Unilever was writing about the cultural forces reshaping personal care whilst its competitor wrote about product formulations and market share. The two companies were each describing their business, but only one was organised around the force that would determine who captured the majority of industry profits.

Power

The shift from a unipolar world to a multipolar one has transformed the operating environment for any firm with international reach. The US-China technology competition is the clearest example. Nvidia must simultaneously serve the Chinese market whilst complying with US export controls that restrict which chips can be sold there. Apple, Tesla, and dozens of other firms face versions of the same constraint. This is a structural realignment, not a trade dispute, and firms caught between the two blocs must now make strategic choices about which markets they can access and at what cost.

Regulatory nationalism reinforces this. Governments are increasingly using regulation as a competitive tool, imposing data localisation requirements, technology transfer conditions, and market access restrictions that fragment what was once a globalising economy. A firm that built its strategy around continued trade liberalisation is operating on a premise that has been weakening for a decade. The theme, stated with enough precision to be actionable, is “the shift toward regulatory nationalism.” Framed that way, a leadership team can allocate resources against it.

My data captured this in an unexpected way. Nokia’s annual reports devoted significantly more language to policy and regulation than Cisco’s over two decades of filings. Nokia oriented toward the rules governing its environment whilst Cisco oriented toward the market transitions reshaping it. The difference preceded the divergence in their profit trajectories by years, which suggests that how a firm relates to Power forces (as constraints to manage or as terrain to navigate) may be a leading indicator rather than a lagging one.

Innovation

The internet was a curiosity when I first encountered it in 1994. The idea that computational technology would create the most valuable companies in the history of capitalism was unthinkable at the time. But it happened, and the content analysis made this force visible with unusual clarity.

Apple’s emphasis on computational technologies was the clearest single signal distinguishing it from HP across 20 years of filings. Apple wrote about software, applications, devices, and systems. HP wrote about toner, laserjet, and printers. Same dictionary of technology language, radically different orientation toward where computing was heading.

Innovation extends well beyond computing. Infrastructure sets the conditions for further change: urbanisation, energy systems, and transport networks transform markets by changing how people live, where they work, and what goods and services can reach them. The continued redevelopment of major cities creates both opportunities and threats for incumbents and new entrants. New transport links, whether roads, railways, or shipping routes, reshape trade patterns and consumer access in ways that take years to materialise but create permanent structural shifts once they do.

Science delivers a different type of innovation from technology. Pharmaceutical breakthroughs, materials science advances, and biotechnology developments create cross-industry consequences that unfold over decades. The forces that reshape industries through innovation are structural rather than sudden, and what matters strategically is whether a firm treats innovation as a feature to add to existing products or as a structural force to organise around. The difference between the two is the difference between a product decision and a strategy.

Nature

Nature operates independently of markets. Climate change, extreme weather, resource depletion, and pollution are structural forces that reshape where people can live, what businesses can operate, and which supply chains survive.

The physical consequences are already measurable. Wildfires, flooding, and rising insurance costs are changing the economics of operating in geographies that were previously viable: major insurers have withdrawn entirely from the California homeowners’ market, and commercial property insurers are repricing risk globally. When the European energy crisis hit in 2022, firms that had treated energy as a background cost discovered it was their most pressing strategic concern. The underlying forces had been visible for years.

Nature also creates markets. Renewable energy, electric vehicles, sustainable agriculture, water management, carbon capture, and climate adaptation services are all industries that exist because of nature-driven change. Treating climate change only as a risk to be managed means seeing half of what is there. The threat and the opportunity are two sides of the same force, and the firms that organised around both early have built positions that late movers will struggle to replicate. Unilever’s decision to build its entire strategy around sustainability, launching the Sustainable Living Plan in 2010, was a bet on this force that competitors categorised as corporate social responsibility rather than competitive architecture. Gilead Sciences offers a less obvious example from the dataset: its annual reports emphasised globalisation and market expansion far more than Amgen’s, but its focus on computational technologies (unusual for a biotech firm) reflected a bet that data-driven drug discovery, sitting at the intersection of Innovation and Nature-driven health concerns, would become a structural advantage. It did.

Economy

The economy is the most familiar force and the one that firms already monitor most closely. Firms do not ignore economic forces. They treat them as background conditions to adjust for rather than structural changes to organise around, and that distinction matters.

A rise in interest rates triggers a review of the capital structure. Recessions trigger cost-cutting. These are responses, not strategies.

Economic forces become strategic themes when they pass the same tests as any other force: sustained structural growth, cross-industry relevance, and actionability. The rise of digital payment systems has been growing for over a decade and affects retail, financial services, logistics, healthcare, and government services simultaneously. A firm could organise its strategy around the shift from cash to digital payments and find applications across its entire portfolio. The growth of emerging-market middle classes, hundreds of millions of consumers entering the middle class for the first time across Asia, Africa, and Latin America, will reshape consumer goods, financial products, healthcare, education, and entertainment for decades. The shift toward subscription-based business models has restructured how value is created and captured across software, media, automotive, and increasingly physical goods. Each of these could anchor a firm’s strategy for a decade or more, which is fundamentally different from treating the economy as a set of conditions to react to quarterly.

Where the forces converge

The most powerful strategic themes sit where two or more forces overlap, and this is where the three-to-four-theme finding from my research becomes most practically useful.

Apple’s emphasis on computational technologies (Innovation) and consumer culture (Society) positioned it at a convergence that HP, focused on business markets and workforce management, missed entirely. Unilever’s emphasis on sustainability (Nature) and consumer behaviour (Society) placed it at a similar intersection. Tesla’s positioning combined electric vehicle technology (Innovation), tightening environmental regulation (Power), falling battery costs (Economy), and consumer preference for sustainable luxury (Society), creating strategic depth that competitors could not easily replicate because they would need to match Tesla across all four dimensions simultaneously.

The three-to-four number emerged from the data rather than from theory. Apple emphasised three driver clusters significantly above HP, and Cisco emphasised three above Nokia. Gilead, operating in a more evenly matched competitive pair, emphasised four above Amgen. Three or four themes is large enough to create a combination that competitors are unlikely to replicate, because it requires simultaneous commitment across multiple domains, yet small enough that the firm can sustain deep commitment across all of them over many years. A single theme creates vulnerability: if the force stalls, the firm has no fallback. More than four creates the same diffusion that conventional strategy produces when it tries to respond to everything.

Scanning a single force in isolation produces observations. Scanning for intersections between forces produces themes.

The practical exercise is to take each of the five forces, identify the drivers within it that are reshaping your industry, and look for the intersections: where do two or three forces overlap in ways that create a structural opportunity or threat?

The answer will differ by firm, even within the same industry. Two firms can pursue the same theme and still compete, because the way each converts the theme into products, processes, and operating decisions creates its own differentiation. But the firms that identify those intersections and commit to building around them over years are the ones that, historically, have captured the dominant share of their industry’s profits.

The SPINE framework is a map. What separates the firms that win from the firms that don’t is whether the forces shape the strategy or sit in a section of the strategy document labelled “external environment” and left there.

That distinction, between monitoring forces and organising around them, is where competitive outcomes are determined.